How Much Inheritance Tax Is your Estate Unnecessarily Exposed To?

Identify hidden risks, reduce unnecessary tax, and protect what ultimately passes to your family

For estates typically above £2m

Delivered within 10-14 days

In many cases, this uncovers avoidable six-figure tax exposure

We’ve reviewed your estate, and there are areas that need to be addressed.

This short video explains the risks we've found, why they matter, and the options available to you.

Who You Will Be Working With

Ranjeet Singh

Chartered Fellow (CISI)

With over 25 years’ experience in the City, including senior FCA-regulated roles, Ranjeet works directly with high-net-worth UK investors on complex estate matters.

A former compliance officer and professional portfolio manager, he has reviewed over 1,000 portfolios and witnessed more than 100 probates.

He is the author of 9 published books and has been a regular commentator on Bloomberg and CNBC for over a decade.

Ranjeet works alongside a network of wealth managers, pension specialists, solicitors, and tax advisers to deliver a coordinated, whole-of-estate approach.

Your Estate Vulnerability Review (EVR)

Findings

Following our initial review, we believe there are weaknesses within your estate that may be increasing inheritance tax exposure and reducing what ultimately passes to your family.

At this stage, these are observations rather than conclusions.

We can see what is happening, but not yet why it is happening, how significant the issue may be, or what options may exist to improve the position.

The purpose of the Estate Diagnostic is to move beyond observation and provide a structured analysis of your property, pensions, investments and estate arrangements.

What You Receive During Your

Estate Diagnostic Assessment

Every estate is different. As part of your Diagnostic Assessment, we carry out a detailed review of your property, pensions, investments, estate structure and long-term planning arrangements.

Rather than providing generic observations, the objective is to identify specific weaknesses, opportunities and implementation pathways relevant to your circumstances.

The reports below represent examples of the type of documentation produced during the diagnostic process.

Your Diagnostic Assessment includes:

The exact reports produced will depend on your circumstances, assets, objectives and the opportunities identified during the review process.

The Real Issue

Most clients we work with already have advisers across tax, legal, and investments. The issue is not usually the quality of advice, but that no one is responsible for how everything fits together.

Each adviser operates within their own area. Decisions are made in isolation, structures are built independently, and gaps begin to form between them.

Over time, these gaps create inefficiencies, increase complexity, and often lead to significant and unnecessary inheritance tax exposure.

There are also critical areas that sit outside any one adviser’s remit, including overall structure, ownership alignment, and how everything ultimately flows through to your family.

When these areas are not addressed properly, the estate may appear organised on the surface, but underneath, it is not working as intended.

This is where estates lose control.

The role of the Estate Diagnostic is to bring everything together into a single, clear framework, allowing you to see what is working, what is not, and where action is required.

Why Timing Matters

The rules around estate planning are shifting, and they are not shifting in your favour.

Recent tax changes, including those following the Autumn Budget 2024, have already impacted many estates, often without people realising. Further reforms, particularly around pensions from April 2027, are expected to bring more assets into scope.

The real risk is not what you can see, but what has quietly changed beneath the surface. In many cases, action is not immediate. Pension and structural adjustments can take months to put in place, and the longer you wait, the fewer options remain, often at a higher cost.

Some choose to wait, hoping future governments may reverse these changes. In practice, this is rare. Over time, rules tend to tighten rather than loosen. Addressing your estate earlier keeps more options available and gives you greater control over the outcome.

The best time to deal with this was years ago. The second best time is now.

What You Will Leave With

By the end of the diagnostic, you will have a clear and structured understanding of how your estate is truly positioned.

You will understand exactly where your inheritance tax exposure is coming from, how it is being created, and which parts of your structure are working against you.

You will know what needs to be addressed immediately, what can be deferred, and how each decision impacts your overall position.

In simple terms, you will leave with clarity, direction and control.

Private Estate Diagnostic (PED)

£2,500

The Estate Vulnerability Review (EVR) establishes that problems exist within your estate. The Private Estate Diagnostic (PED) determines how that problem can be solved.

We assess potential solutions, quantify the likely benefits, estimate implementation costs, and where appropriate, engage relevant specialists to consider alternative approaches.

The result is a practical implementation blueprint showing what should be done, who should do it, and what it is likely to achieve.

Already Working With Advisors?

Most families we work with already have advisers.

Solicitors prepare Wills, accountants focus on tax and wealth managers typically oversee investments.

The challenge is that very few professionals are responsible for ensuring everything works together as a single estate strategy.

The Estate Diagnostic is not intended to replace your existing advisers. Instead, it acts as an independent second opinion, identifying gaps, challenging assumptions and providing a framework that existing advisers can work from.

Some families use the Diagnostic to gain clarity and then continue working with their existing advisers.

And some families choose to implement the plan with us, using our team of regulated advisers.

Our Guarantee

Most estates of this size contain material inefficiencies, missed allowances, or structural gaps.

As a result, we expect the value identified through this diagnostic to significantly exceed the cost of the engagement.

If we are unable to identify meaningful financial or structural opportunities to improve your position (typically £20,000+ in potential impact), your fee will be refunded in full.

Your Next Step

This isn’t just about saving tax, in some cases several hundred thousand pounds or more.

It’s about giving your family clarity and peace of mind, reducing the risk of confusion or conflict, and putting everything in order while you can.

For clients who have completed the diagnostic, the biggest surprise is often the sense of clarity and reassurance it provides.

So that no one is left trying to piece things together when you’re no longer here.

One-time diagnostic. No ongoing commitment required.

A limited number of estate diagnostics are taken on each month due to the depth of analysis required. Where capacity is reached, the next available opening will be offered.

Premium Diagnostic (£5,000)

For clients who prefer a more tailored approach and faster turnaround.

Both the Standard and Premium options follow the same structured diagnostic process. The Premium option simply provides a more tailored experience and an accelerated delivery timeframe.

Includes everything in the standard diagnostic, plus:

1. Priority Turnaround

Delivered within 5 working days

(Standard: 10–14 days)2. Two Diagnostic Reports

Client version (clear and simplified)

Adviser version (structured for implementation)

3. HMRC 6-Month Review Window

If there are any material HMRC changes, we will revisit the report free of charge.

This option is typically selected by clients who require a faster turnaround, or wish to use their own advisers to implement the diagnostic plan.

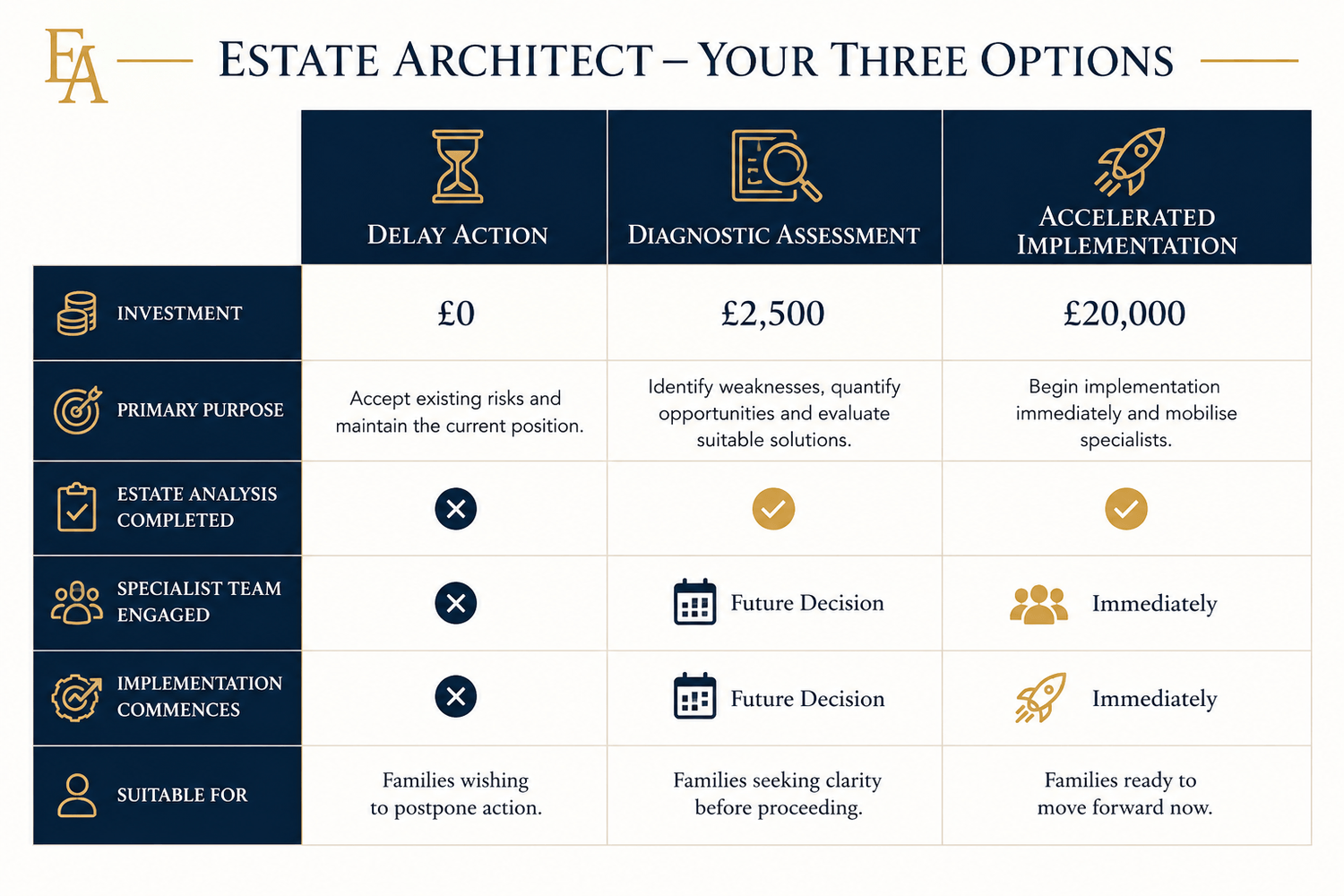

Three Ways Forward

Following your Estate Vulnerability, there are three possible routes available.

Option 1 – Do Nothing

£ FREE

This is generally the least attractive option.

You already know there are weaknesses within your estate structure, and doing nothing simply allows those weaknesses to remain in place.

In many cases, estates continue to increase in value over time. A larger estate can mean a larger inheritance tax liability, reduced planning flexibility and fewer available options.

Tax legislation can also change. Pension rules are already scheduled to change from April 2027, and future Governments may alter allowances, exemptions and reliefs further.

Delaying action may also mean paying higher professional fees in the future, waiting longer for specialist availability and facing a more complex estate to reorganise later.

Whilst this option costs nothing today, it may ultimately prove to be the most expensive decision.

Option 2 – Diagnostic Assessment

£2,500

(£1,250 upon instruction and £1,250 upon completion)

This is the route chosen by most families.

The Diagnostic Assessment is designed for those who would like complete clarity before committing to implementation.

It identifies precisely what should be done, who should do it, what it is likely to cost and the potential tax savings that may be achievable.

Included within the Diagnostic Assessment

✔ Comprehensive review of your estate structure

✔ Identification of weaknesses and planning opportunities

✔ Property, pension, investment and business analysis

✔ Indicative inheritance tax modelling

✔ Input and quotations from appropriate specialists

✔ Detailed written report of approximately 40–50 pages

✔ Private presentation meeting lasting approximately 60–90 minutes

Option 3 – Implementation

£20,000

(£10,000 upon instruction and £10,000 upon completion)

For families who already know they wish to take action and would prefer not to make two separate decisions.

The diagnostic work is still undertaken internally as part of the process. However, instead of stopping after the analysis stage, we immediately mobilise the relevant specialists and begin implementation.

Potential advantages of implementation:

✔ Planning begins immediately rather than several weeks or months later

✔ Specialists can be engaged sooner, helping secure availability and current fee structures

✔ Estates may be easier to reorganise before they increase further in value

✔ Current legislation and available reliefs may be utilised before future changes take effect

✔ A single engagement process rather than a two-stage decision

✔ Dedicated project management throughout the implementation period

Typical implementation projects include

✔ Property restructuring

✔ Pension planning and beneficiary reviews

✔ Trust creation and wealth transfer strategies

✔ Investment and wrapper optimisation

✔ Probate liquidity planning

✔ Coordination of solicitors, accountants and other specialists

Implementation projects typically take between 6 and 9 months to complete.

Implementation is suitable for families who already know they wish to resolve the issues identified and would prefer not to delay matters by making two separate decisions.

By commencing immediately, specialist availability can often be secured sooner, planning opportunities can potentially be implemented under current legislation, and estates can frequently be easier to reorganise before they increase further in value.

Some planning opportunities rely on surviving a number of years.

The earlier planning commences, the earlier those clocks start running.

Estate Architect provides educational research and analysis relating to inheritance tax and estate planning concepts for UK residents. We do not provide regulated investment, tax, or legal advice and are not authorised or regulated by the Financial Conduct Authority (FCA). Where regulated advice is required, introductions may be made to authorised professionals.

© Estate Architect 2026