HMRC Could Take 40% Of Everything You Spent A Lifetime Building

Most families already have advisers.

Very few have an estate structure.

✓ Takes 2 minutes

✓ Immediate findings

✓ No obligation

NEW BOOK RELEASE

I Thought I Was Sorted

You Don't Have A Tax Problem

You Have A Planning Problem

You worked a lifetime to build your wealth.

Don't let poor planning decide who receives it.

Paperback Retail Price £29.99

Why Your Family Is At Risk

Inheritance tax was once seen as a problem affecting only the very wealthy.

That is no longer true.

Rising property prices, growing pensions and long-term investment growth mean many ordinary families have already drifted into inheritance tax territory.

A family home.

A pension built over decades.

A carefully managed ISA portfolio.

Individually, these are not unusual.

But together, they can create a significant inheritance tax problem.

The issue is that your wealth continues to build in your personal name, and it keeps growing every year.

As a result, your children are now more likely than ever to face inheritance tax, probate delays, pressure to sell assets and unnecessary stress.

The 2027 Pension Tax Shock

The Autumn 2024 Budget marked one of the biggest inheritance tax changes in a generation.

For years, pensions were treated as sacred. They were seen as one of the safest and most tax-efficient ways to pass wealth to the next generation.

That is now changing. From April 2027, SIPPs and some pensions will be included within your estate for inheritance tax purposes.

The impact is significant. Pensions are often the second largest asset after the family home. Even worse, pension wealth could face both inheritance tax and income tax. A double taxation problem.

This could create an effective tax rate of up to 67%.

Two-thirds of your pension lost in tax.

After decades of being encouraged to build pension wealth, families are now asking a simple question:

What can be done about it?

Understanding the 2027 Pension Changes and Their Impact on Estates

Download the Inheritance Tax Report to explore how structured planning may help families navigate the evolving rules.

Inside this report, you’ll find:

An overview of the proposed 2027 pension changes

How inheritance tax interacts with pension wealth

Common estate structuring considerations

A practical framework for thinking about long-term family wealth

Prepared by Ranjeet Singh BA MSc FCSI, this report provides clear, structured commentary drawn from over two decades of experience in financial markets.

The Moment Everything Changed

After more than 25 years as an FCA-regulated investment manager, reviewing thousands of investment portfolios and working with high-net-worth families, I began noticing the same pattern again and again.

It had been my job to help families grow wealth through ISAs, pensions and investments.

And I did.

But after death, large portions of that wealth were suddenly lost through inheritance tax.

And the loss wasn’t just financial.

Children fell out.

Assets were sold in fire sales.

Families were ripped apart.

In many cases, wealth that took a generation to build disappeared surprisingly quickly.

I couldn’t understand why.

My clients had some of the best advisers in the country.

Accountants. Lawyers. Financial planners.

So it wasn’t a lack of advice.

Something else was missing.

Eventually I realised what it was.

The advice was fragmented. Disconnected.

Their advisers were doing everything correctly, but nobody was responsible for the estate as a whole.

This wasn’t the fault of the advisers. It simply wasn’t their role.

That’s when I realised every family needed one thing: An Architect.

Someone responsible for bringing the entire plan together.

That was the moment Estate Architect was born.

And that is what you're missing.

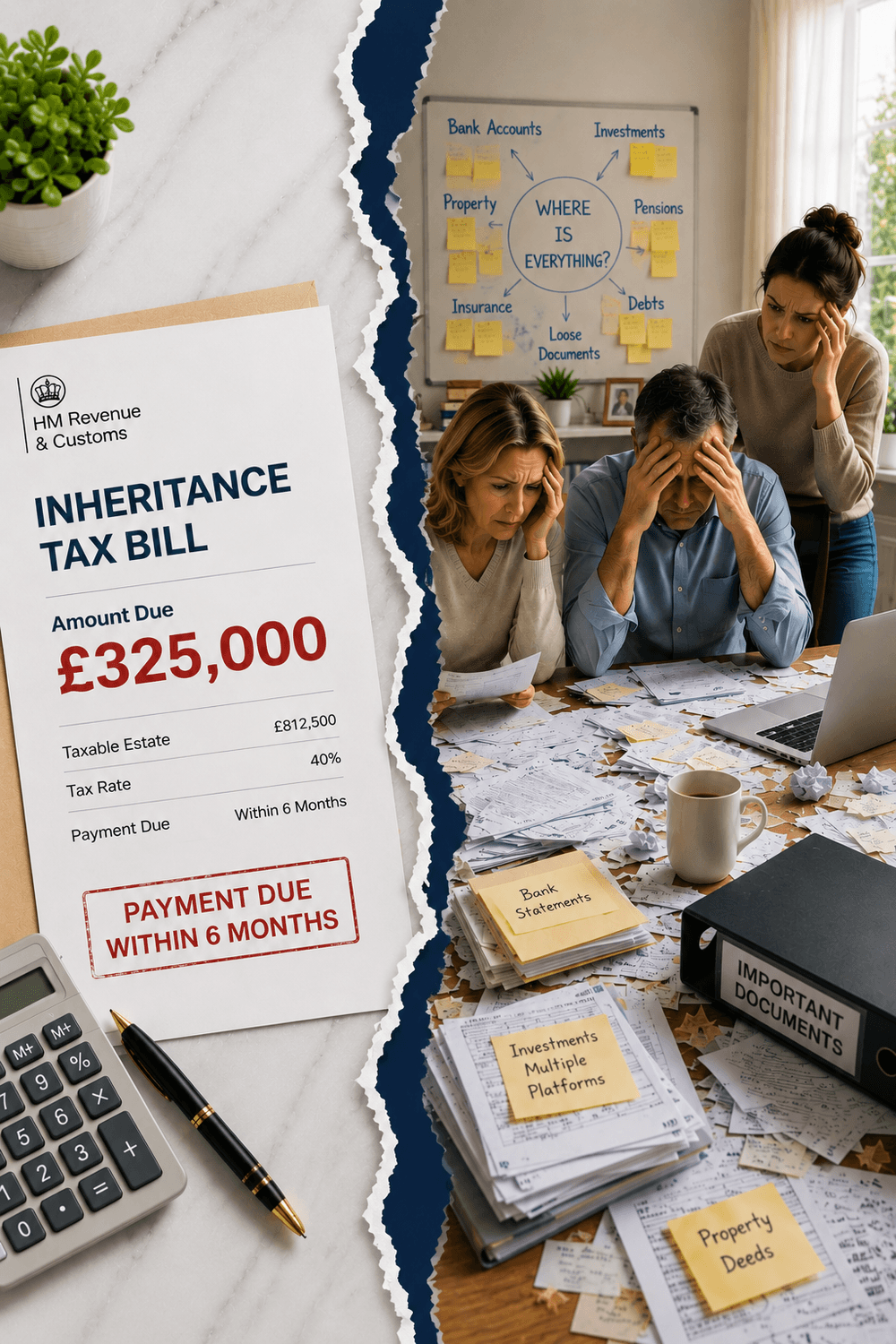

Inheritance Tax Is Only Half The Problem

Most families think the tax bill is the problem. It isn't.

The bigger issue is the confusion, stress and disorder left behind for the family.

Missing paperwork. Unclear instructions. Multiple advisers. Different platforms. Assets scattered everywhere.

At the exact moment your loved ones are grieving, they are suddenly expected to piece everything together.

That is where estates begin to unravel.

Children fall out.

Mistakes get made.

Deadlines get missed.

Inheritance tax usually needs to be paid to HMRC within six months.

But most families are woefully unprepared.

And out of the estates I have reviewed, almost without exception, they were poorly organised.

It was never just about protecting wealth. It was about creating certainty for the family left behind.

Because the greatest gift you can leave your family is not just wealth.

It is peace of mind.

Powered by the Estate Master Key System™

HMRC Defence Vault™

Digital Estate Register™

Family Continuity Network™

Executor Action Guide™

Probate Liquidity Framework™

Estate Master Key Portal™

Protecting wealth is only half the job. Organising everything around it matters too.

The Retirement Dilemma

Most families face the same problem. They sit between two fears.

Give too much away too quickly, and they worry about running out of money, losing control, making gifting mistakes, or reducing their own lifestyle. Give away too little, and they risk leaving behind a larger estate exposed to inheritance tax.

And nobody knows what tomorrow looks like. Children can divorce. Circumstances can change. Care needs can arise.

Life rarely follows a perfect plan.

That is why estate planning should never begin with one question: "How much can I give away?"

It should begin with a different question: "How do I protect my own lifestyle first?"

Because before protecting your children, you need to protect:

✓ Your income

✓ Your lifestyle

✓ Your holidays and retirement plans

✓ Future care needs

✓ Financial flexibility and control

The goal is not to give everything away.

The goal is to create the right structure.

One that helps you enjoy life today, while protecting your family tomorrow.

Because estate planning is not just about what happens after death.

It is about living well first.

Everybody Thinks Their Estate Is "Fine"

Imagine a couple in their late 60s or early 70s.

They own a family home.

They have pensions, ISAs and investments.

They have children and grandchildren they want to protect.

On paper, everything looks sensible.

They already have wills.

They already use an accountant.

They already have a financial adviser.

And that is exactly why many people assume everything is 'sorted'.

But after reviewing hundreds of estates, I have learned something:

What we don't know can be expensive.

Out of every 10 estates I review, at least 9 typically have weaknesses.

Not because advisers have done anything wrong.

It's simply because no one has looked at the entire structure.

Did you know…

✓ A lost Residence Nil Rate Band (RNRB) can be recovered?

✓ The Spousal Buffer Strategy™ is affected by divorce?

✓ Assets concentrated in one spouse's name weaken your estate?

✓ Illiquid investments can create major probate delays?

✓ A Probate Liquidity Fund (PLF) helps families access instant capital?

✓ A Life Insurance Limited Company Strategy™ can pay the tax bill immediately?

✓ A Trust Gifting Framework™ improves long-term planning flexibility?

✓ An Estate Shareholder Agreement™ reduces future family conflict?

Most families and even advisers, have never heard of these concepts.

That’s why you need somebody to review your estate from a different perspective.

Not just a general adviser, but an Estate Architect.

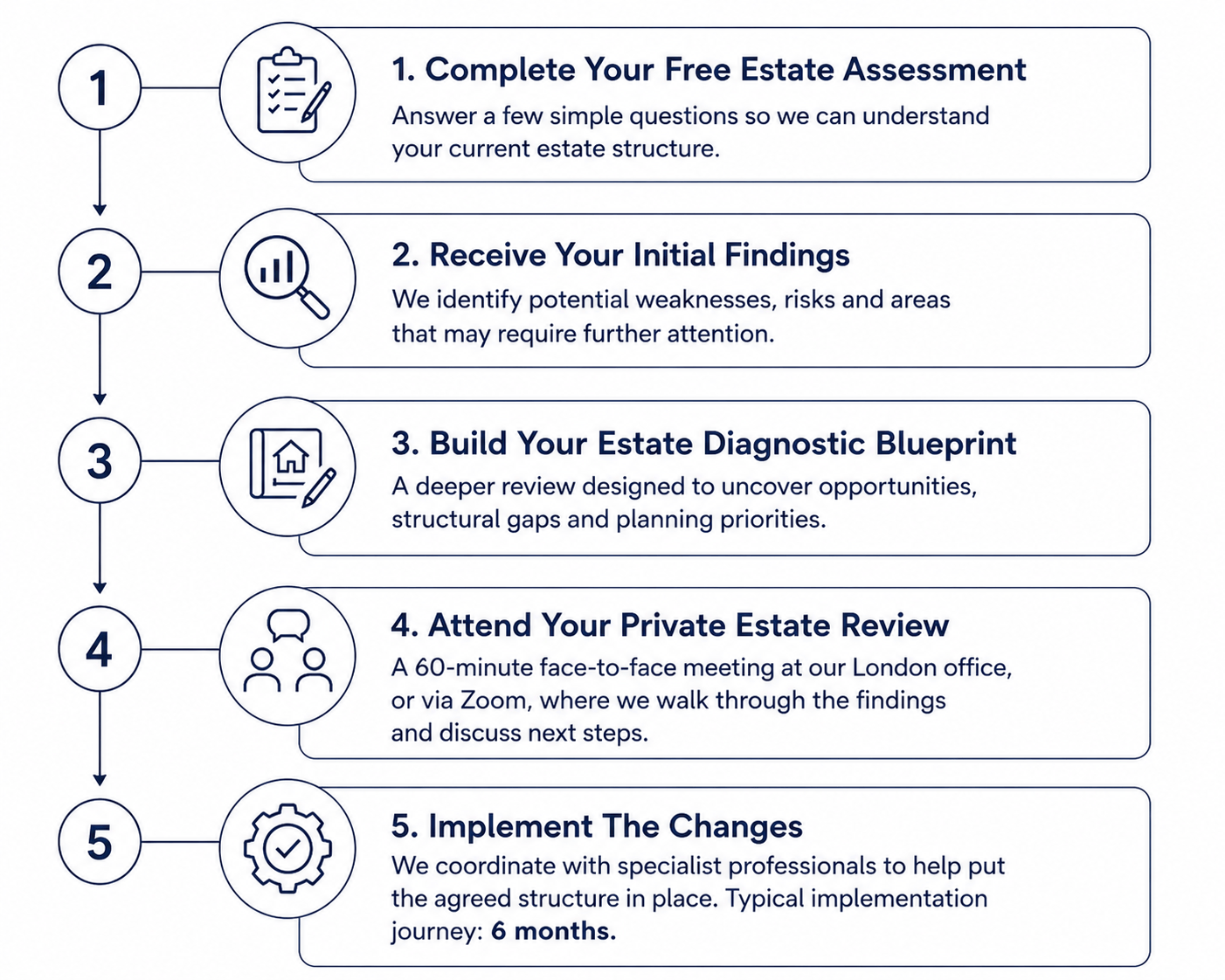

How It Works

Time Is Running Out

For years, inheritance tax was seen as something affecting only the very wealthy.

Today, more families are being pulled into the system every year.

One reason is simple.

The Nil Rate Band has remained frozen since 2009 and is expected to stay frozen until 2031, while property prices, pensions and investments continue to rise.

This is a stealth tax.

Your estate keeps growing, while the thresholds stay the same.

Recent pension changes have also made one thing clear.

Inheritance tax is firmly on the Government’s agenda.

And few people would be surprised if future Budgets bring further changes.

At the same time, more families are now looking for planning solutions. As demand increases, options are becoming more limited and implementation costs are rising.

Waiting rarely makes estate planning easier.

Because every year:

✓ Asset values continue to grow

✓ Tax exposure is increasing

✓ Rules are making it harder

✓ Opportunities are narrowing

✓ Planning is becoming more expensive

The good news is that the Government rarely applies changes retrospectively.

That means structures put in place today can help protect your family tomorrow.

You have a choice.

Either spend your wealth faster than it grows, which still does not solve the property inheritance tax problem.

Gift too much away too quickly and risk reducing your own lifestyle.

Or create a structure that protects you now and your children in the future.

✓ Takes 5 minutes

✓ Immediate findings

✓ No obligation

Estate Architect provides educational research and analysis relating to inheritance tax and estate planning concepts for UK residents. We do not provide regulated investment, tax, or legal advice and are not authorised or regulated by the Financial Conduct Authority (FCA). Where regulated advice is required, introductions may be made to authorised professionals.

© Estate Architect 2026

Arrange a Conversation

If you have clients with more complex planning needs, we are happy to have a short initial conversation. We will identify key gaps and outline how a more coordinated approach may help.

No obligation. Practical and focused.

We will respond personally and arrange a suitable time.

Estate Architect provides estate structuring and coordination services and does not provide regulated financial advice. Any planning discussed is subject to further professional review and formal engagement. All services are instructed and billed separately.

By submitting this form, you agree to be contacted by Estate Architect and to receive relevant information, updates, and occasional marketing communications. You can unsubscribe at any time.

Refer a Client

If you have a client whose affairs extend beyond routine tax work, you can introduce them for a structured review.

We will assess the situation, identify key gaps, and coordinate the appropriate next steps, while keeping you informed throughout.

Estate Architect provides estate structuring and coordination services and does not provide regulated financial advice. All client engagements are subject to direct instruction and agreement.

By submitting this form, you confirm you have permission to share the client’s details and agree to receive relevant information, updates, and occasional communications from Estate Architect. You can unsubscribe at any time.

We HATE spam. Your email address is 100% secure